Someday, maybe Illinois Republicans and conservatives will wake up to the fact about government employee pension promises. Hear are Ted Dabrowski and John Klingner from back in August:

You can trust public pension apologists to deflect any critique that calls out the failure of defined benefit plans. Unsurprisingly, their response to a recent Wall Street Journal editorial highlighting Wirepoints’ research was just that – deflection via misdirection and victim playing.

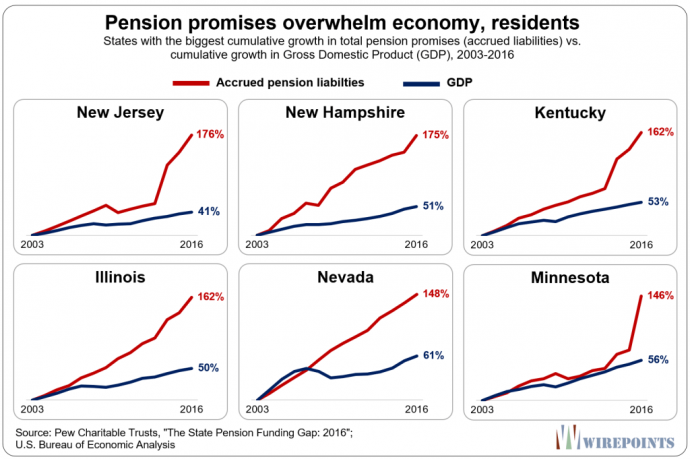

Wirepoints found that a skyrocketing growth in pension benefits, what are known as accrued liabilities, is behind most of the state pension crises playing out across the country. Uncontrolled pension benefit growth is swamping many state economies and the residents who pay for those benefits.

The apologists find the facts inconvenient, so they deflect. They revert to their standard narrative that state governments, and by extension taxpayers, are to blame for “failing to fully fund their public pension commitments.” Or that public employees are the only “victims.” Or they criticize unessential details to distract from the undeniable growth in benefits.

But the apologists don’t disprove the core findings of our research: that unrestrained benefit growth is behind many state fiscal crises.

That was the subject of our two most recent reports: Illinois state pensions: Overpromised, not underfunded and Overpromising has crippled public pensions: A 50-state survey.

The numbers are undeniable. And it’s not just the growth rate of accrued liabilities that’s daunting. It’s how they’re crowding out everything in their path.

Pensions are a drag

Some public pension apologists took issue with the following graphic. They complained that comparing the growth of total pension benefits (accrued liabilities) to the growth in other economic indicators like GDP is “illogical and has no theoretical basis.”

That’s an absurd argument.

The fact is accrued liabilities are a debt – they are the sum of every pension obligation made to all workers and retirees. The growth in that debt over time matters since taxpayers are liable for a large chunk of those promises. If the sum of those promises grows too fast year after year – far faster than an economy (GDP) and its taxpayers (household incomes) can keep up with – a shortfall will invariably occur.

Read more: Wirepoints